←

All posts

How Nook Leverages DeFi Lending to Grow Your Savings

Published

Apr 1, 2025

Written by

Joey Isaacson

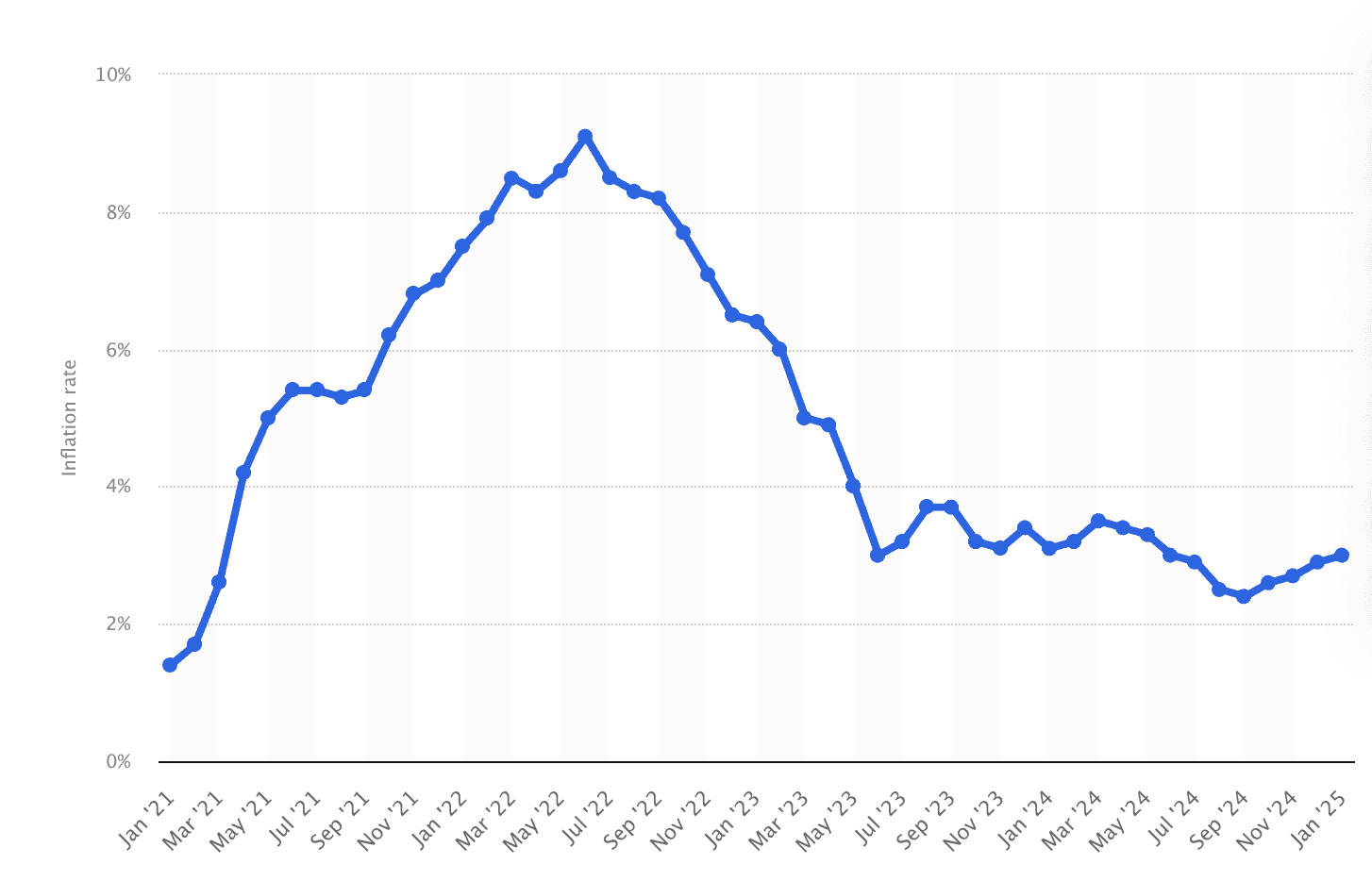

If you feel like you’re not getting ahead with your traditional savings account, you’re not alone. Most banks keep 80–90% of the profits they generate with your deposits - passing only a fraction back to you. As of March 2025, the national average savings rate in the U.S. is just around 0.5%, while inflation averages around 3%, after peaking above 9% in mid-2022. That substantial gap means money kept in traditional savings accounts is quietly losing value and purchasing power year after year.

Nook is a savings platform powered by decentralized finance (DeFi) lending. It’s how we generate the interest you earn in the app. Behind the scenes, your deposits are routed to secure, 100% collateralized lending protocols where they start earning immediately. You don’t need to know anything about DeFi or Crypto to benefit from it.

We built Nook to offer you a better alternative to traditional savings accounts. Our mission is to help you to actually get ahead with your savings by making DeFi lending simple, accessible, and secure.

The charts below highlight the gap between inflation rates and average bank savings rates over the past five years.

Inflation rates

source: https://www.statista.com/statistics/273418/unadjusted-monthly-inflation-rate-in-the-us/

National bank savings rates

source: https://fred.stlouisfed.org/series/SNDR

What Is DeFi Lending?

Decentralized Finance, or DeFi, is a blockchain-based financial system that operates without the need for traditional intermediaries like banks.

DeFi lending lets you earn interest on your money by lending it to people who deposit cryptocurrencies like Bitcoin and Ethereum as collateral. Borrowers use these protocols to access funds without selling their crypto, paying an interest rate in return.

How does it work?

Nook is built to help your money grow without constant management or the need to bet on volatile markets. Instead of investing in stocks or navigating crypto trades, your deposits are routed through trusted DeFi lending protocols like Moonwell, where they start earning interest immediately.

These protocols don’t use banks or brokers. They run on smart contracts - code that enforces loan terms without human involvement. Borrowers lock up more than they borrow - (e.g.,$15,000 in Bitcoin to access $10,000).

Once the loan is live, the contract handles everything: repayments, collateral management, even liquidations if values drop too far. If the borrower pays back, their collateral is returned. If not, it’s sold to cover the loan - keeping lenders (Nook users), protected.

Interest rates fluctuate based on supply and demand. When borrowing activity is high, yields increase. When it slows, rates adjust down. In 2024, Moonwell lending averaged 9.34% APY - 20x above the average national savings rate and even higher than most “high-yield” options like Robinhood’s 4%.

If the rate ever dips below your comfort level, you’re not stuck. There are no lockups, penalties, or delays. You can withdraw anytime - directly to your bank. Unlike traditional accounts that pay interest monthly, Nook lets you earn (and access) yield in real time.

Safety and Risk Management

Safety in DeFi works differently than in traditional finance. There are no banks acting as gatekeepers and no insurance backing your deposits. Instead, protection is built into the structure of the system itself.

At the core of it is the aforementioned over-collateralization. Borrowers are required to deposit more than they borrow. If the value of the collateral drops too far, the protocol liquidates the position automatically, paying back the loan and shielding the lending pool from loss.

All of this is enforced by smart contracts and doesn’t rely on trust or manual approvals. It just executes. And because the code is public, anyone can review it. Many of the leading protocols undergo regular third-party audits to catch vulnerabilities before they become problems. Moonwell, Nook’s partner protocol, has never experienced a security breach and also maintains a $250,000 bug bounty as a safeguard.

Still, this isn’t a bank. There’s no FDIC protection, no customer support hotline to reverse a bad decision. What DeFi offers instead is transparency, automation, and architecture that’s been tested - and continues to operate without centralized control.

Historical Market Trends

DeFi lending didn’t appear overnight - it’s been a steady evolution. The earliest wave, from 2018 to 2020, was mostly experimental. Projects like MakerDAO introduced the foundational ideas: decentralized borrowing, on-chain collateral, and smart contract enforcement. It was niche, highly technical, and largely ignored by the broader financial world.

Then came the acceleration. Between 2020 and 2022 - what many call “DeFi Summer” - usage exploded. Platforms like Aave and Compound brought more liquidity, better interfaces, and a surge of participation. What was once a fringe movement became one of the most active sectors of the DeFi ecosystem.

Since 2023, regulation has become clearer, institutions have started to pay attention, and the protocols themselves have matured and further improved their security. As a result, mainstream adoption followed. From 2023 to 2025, the number of DeFi lending users grew from 5.5 million to 7.8 million - a 41.8% increase.

Market projections suggest this is just the beginning. By 2031, the overall DeFi market could reach over $350 billion, growing at a compound annual rate of nearly 49%. This is driven by infrastructure that’s finally ready for the mainstream, as well as the US government starting to embrace Crypto/DeFi technology and innovation. (Source: https://www.kbvresearch.com/press-release/decentralized-finance-market/).

Current Market Analysis

As of early 2025, DeFi lending maintains steady growth and institutional support:

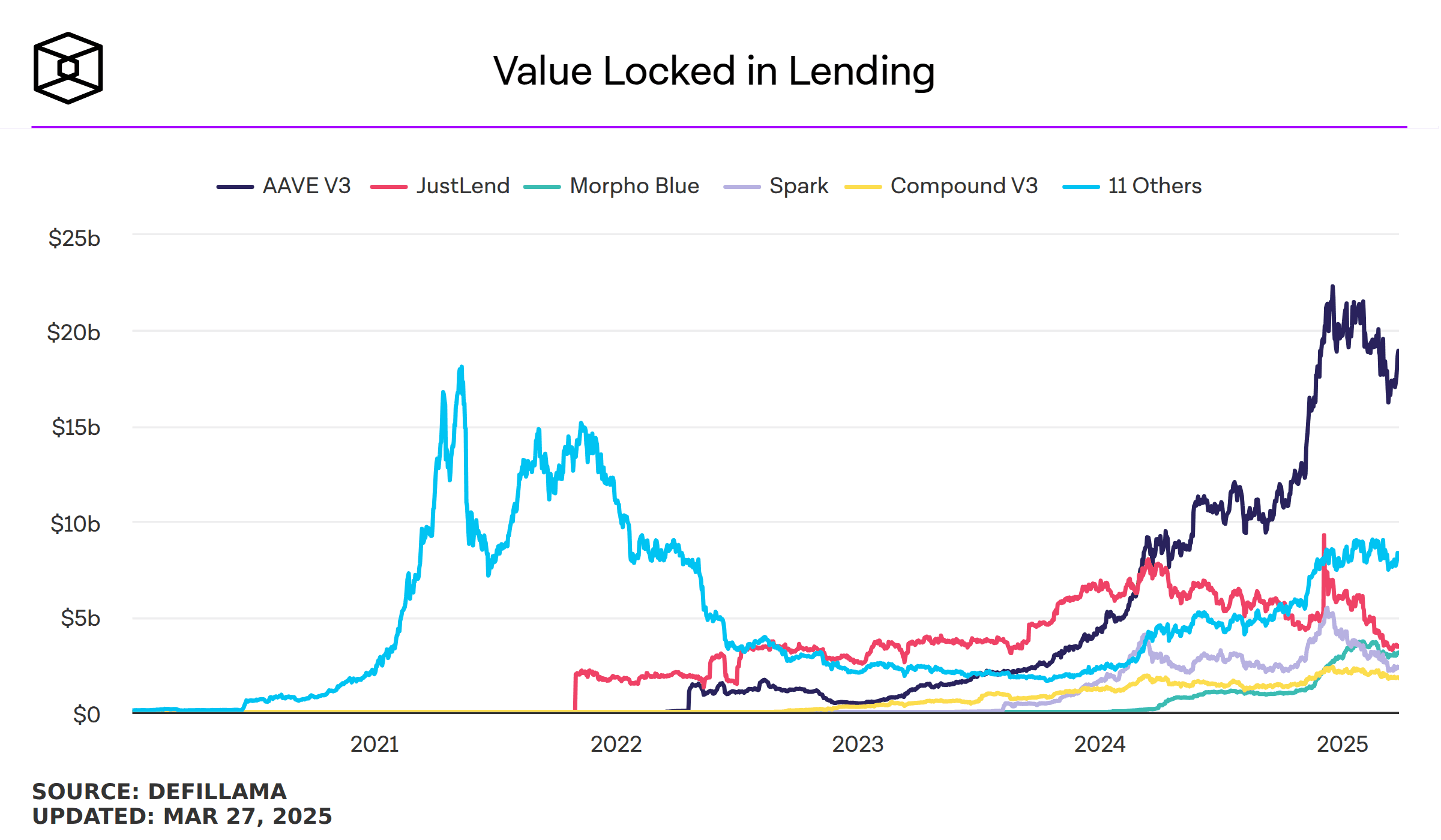

Total Value Locked (TVL): Approximately $32 billion in assets are locked in lending protocols as of March 2025.

Leading Platforms:

Aave: Approximately $18 billion TVL, known for diverse assets and strong institutional backing.

Moonwell: Approximately $120 million TVL, known for strong security, regular audits and a $250,000 “bug bounty”.

Below is a chart showcasing the TVL in DeFi lending. Adoption started picking up in mid 2020 and entered a steep overall uptrend starting in 2023.

How to Get Started

Getting started with Nook is simple. There’s no need to understand crypto or manage anything manually. You can go from sign-up to earning interest in just a few minutes - here’s how →

Step one:

Fund your account using Apple Pay, a debit card, or your Coinbase account. The minimum is just $5. Once funds are deposited, they are automatically deployed to audited DeFi lending platforms where they begin earning interest immediately.

Step Two:

Your funds are lent out through the aforementioned protocols. Everything runs on secure, audited smart contracts. You don’t have to manage or monitor anything.

Step Three:

Withdraw anytime, with no penalties or delays. Your funds are sent straight to your linked bank account via ACH. And because your money stays in your self-custody wallet, you remain in control.

If you have further questions about how Nook works and want to dive deeper, please feel free to join our public Telegram group and connect with the team. We’re more than happy to hop on a call with you and address any questions you may have: https://t.me/nooksavings. You can also reach out to us at support@nookapp.xyz.

Sources: https://defillama.com/ , https://www.kbvresearch.com/ , https://cointelegraph.com/ , https://www.statista.com/ , https://aave.com/ , https://moonwell.fi/discover